THO STRATEGIC INTELLIGENCE

EXECUTIVE BRIEFING | GLOBAL WORKFORCE & PROFESSIONAL SERVICES | MULTI-CONTINENTAL ANALYSIS

The Global Talent Reckoning: A Crisis Without Borders

How a simultaneous professional services workforce collapse across the United States, United Kingdom, Australia, and Canada — combined with AI displacement, Asia’s dominant outsourcing infrastructure, and Nigeria’s landmark tax reform — is forcing a fundamental redesign of how global economies source, develop, and govern expert professional labour.

Date of Issue: 21 March 2026 | Classification: Strategic Restricted

| 6 Nations Simultaneous shortage US, UK, Australia, Canada, Ireland, NZ | $55B Global FAO market 2025 Projected $81B by 2030 (CAGR 9.3%) | 1.6M India finance professionals Global Capability Centres, 2025 | 92M WEF: jobs displaced by 2030 Accountants among fastest-declining roles |

Executive Summary

This briefing synthesises data across six major economies and five continents to present a thesis that should concern every strategic leader: the professional services workforce crisis is not a US problem, a UK problem, or an Australian problem. It is a simultaneous structural failure in every high-income economy, playing out at the same moment that AI is eliminating the training pathway through which the next generation of senior professionals would have qualified. The convergence of these forces is being met by a global outsourcing infrastructure — led by India and the Philippines — and, most recently, by a sovereign policy innovation from Nigeria that signals a new era of deliberate talent liberalisation.

[O1] [O2] is a paradox engine, not a solution. The World Economic Forum’s Future of Jobs Report 2025 lists accountants and auditors among the fastest-declining occupations globally by 2030. Yet vacancy rates are simultaneously at all-time highs in every market surveyed. AI eliminates the entry-level roles that form the professional pipeline — making the long-term shortage worse even as it improves short-term throughput.

Leaders who treat these as separate HR or technology issues will be outpaced. The strategic imperative is to act on the convergence — redesigning talent architecture, governance frameworks, and international sourcing partnerships for a structurally different professional landscape. |

SECTION 01 | THE UNIVERSAL COLLAPSE

Six economies, one simultaneous crisis

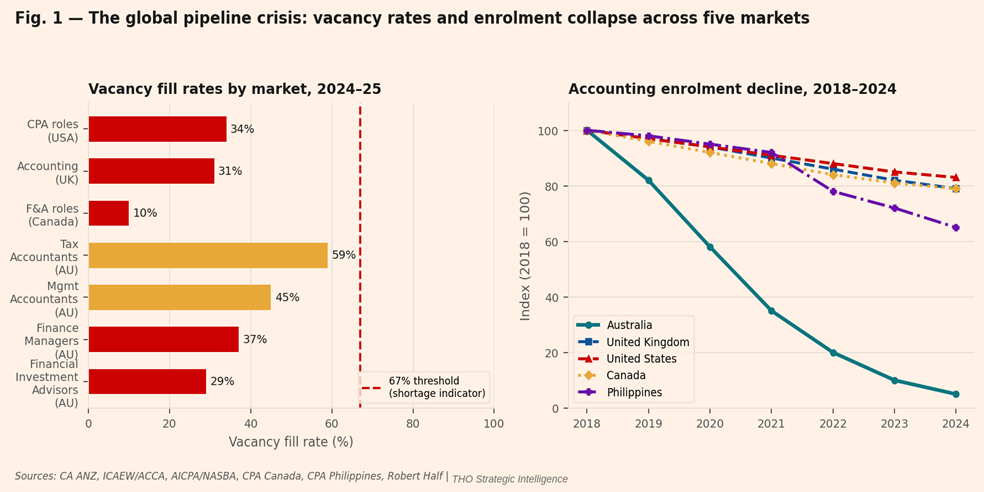

Fig. 1 The global pipeline crisis: vacancy fill rates and enrolment collapse across five markets

Left: vacancy fill rates by occupation and market (2024-25); the 67% threshold marks where Jobs & Skills Australia defines a shortage. Right: professional accounting enrolment indexed to 2018=100. Australia’s 95% collapse is without parallel. Data: CA ANZ, ICAEW/ACCA, AICPA, CPA Canada, CPA Philippines, Robert Half, THO Strategic Intelligence.

What makes this moment historically distinctive is not that one country is short of accountants. It is that every high-income economy is short of them, simultaneously, for the same structural reasons, with no credible domestic remedy in sight.

In the United States, the AICPA describes a full pipeline crisis. Licensed CPA numbers stand at 653,408, down from a peak above 1.93 million for the broader accounting and auditing workforce. CPA exam candidates have fallen 43% from their 2010 peak. Over 90% of finance and accounting hiring managers report difficulty filling roles.

In the United Kingdom, the picture is structurally identical. Skills England has identified accounting and finance technicians among the top ten most critically in-demand occupations in the country — alongside care workers and transport directors — with 994,000 finance sector workers needed. From 2017 to 2022, ICAEW, ACCA, and CIMA collectively enrolled 9,000 fewer students. The average age of a UK accountant is 46. Brexit has compounded the shortage by removing approximately 330,000 workers from the UK labour market, including a material share of accounting professionals who held EU-member-state qualifications.

|

AUSTRALIA: THE MOST SEVERE PIPELINE COLLAPSE ON RECORD Enrolments in Australia’s Accounting Professional Year Programme — the structured pathway from qualification to workforce entry — fell from 7,122 in 2018 to just 340 in 2024. A 95% collapse in six years. CA ANZ has found ongoing shortages across 11 accounting, audit and finance-related occupations. Vacancy fill rates sit below 29% for financial investment advisers and 37% for finance managers. The profession is calling for urgent government intervention, including placement on the National Skills Occupation List. |

Canada mirrors the trend with its own specific pressures. CPA Canada has warned that accountant shortages will have long-term consequences for financial stability. BNN Bloomberg reported in April 2024 that 90% of Canadian finance and accounting hiring managers were struggling to fill positions. A 12% decline in full-time accounting professors has eroded the academic pipeline. Ireland has declared accounting a critical national skill shortage and opened emergency skilled visa pathways.

The common cause of this multi-continental failure is not a mystery. The accounting profession faces the same demographic reckoning in every market: an ageing core cohort approaching retirement simultaneously with declining graduate enrolments, as technology competition, perceived career limitations, and the cost of qualification deter younger entrants. Where the United States requires 150 credit hours for CPA qualification, Australia requires completion of a Professional Year Programme, and the UK requires ICAEW, ACCA, or CIMA chartership — each of these pathways now faces the same perception and cost barriers that are driving graduates toward fintech, data analytics, and software engineering instead.

| PRIVATE SECTOR EXPOSURE Organisations with significant US, UK, Australian, or Canadian accounting function footprints are operating with compounding vacancy risk. The probability of a material weakness event linked to accounting staff turnover is rising in all four jurisdictions simultaneously.Salary inflation is accelerating as firms compete for a shrinking pool. Robert Half reports 8% average CPA salary increases in Canada in 2024; CA ANZ documents a 7.6% pay rise in Australia — both well above general wage growth, and continuing to accelerate.The perception that this is a temporary post-COVID phenomenon must be explicitly corrected at board level. The demographic and enrolment data indicate a structural shortage persisting through at least 2030 in all six affected markets. | PUBLIC SECTOR EXPOSURE Revenue agencies, national audit offices, and central banks face the same pipeline failure as the private sector but compete for the same talent at lower salary bands. In most cases, they are losing.Ireland’s declaration of accounting as a critical skill shortage is the most visible example of a government recognising that the professional infrastructure underpinning its tax system and audit regime is at risk. Similar formal risk assessments are overdue in the UK, US, Australia, and Canada.Governments that have not yet conducted workforce vulnerability assessments for their own finance functions are operating with unquantified institutional risk. |

SECTION 02 | THE ASIA EQUATION

India, the Philippines, and two decades of supply-side architecture

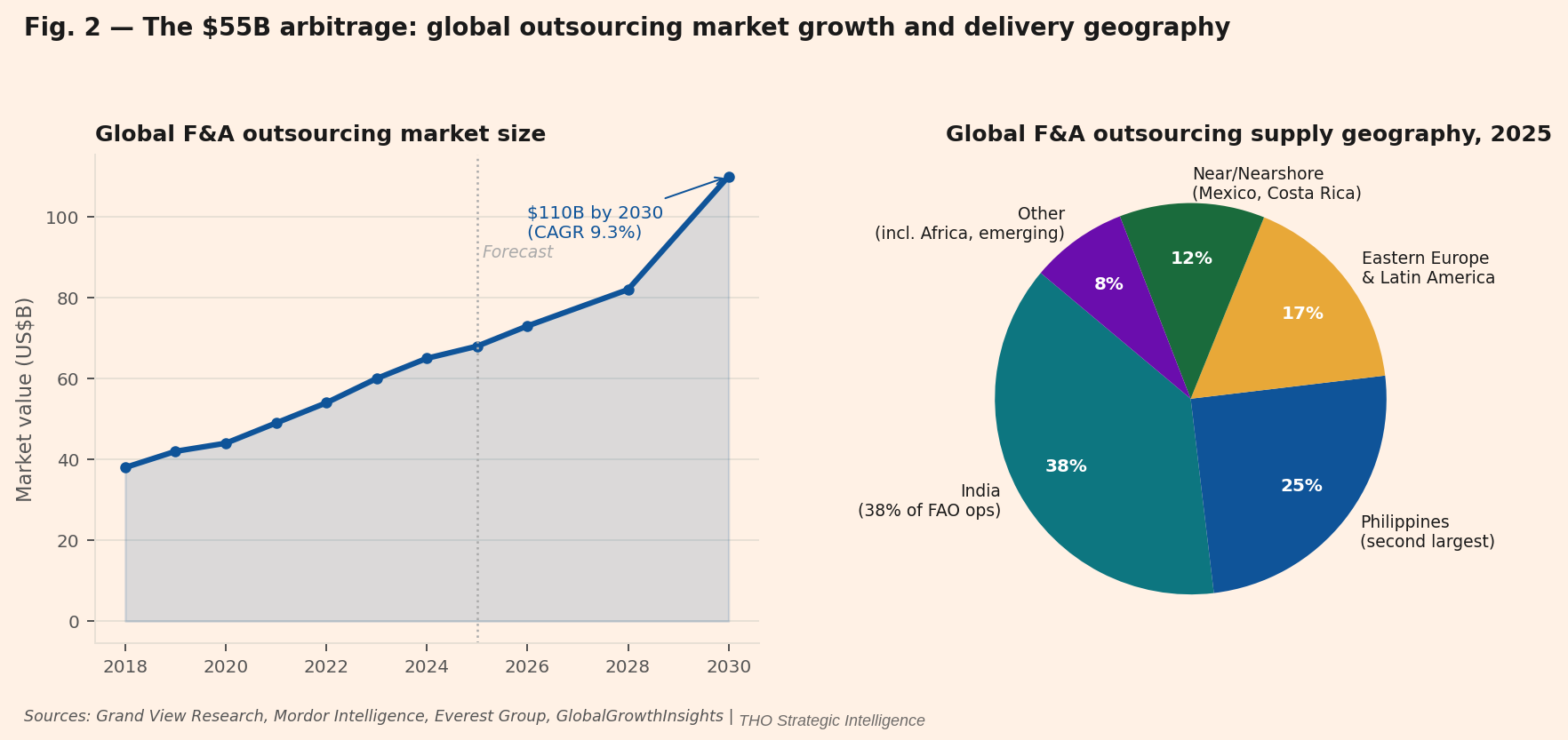

Fig. 2 The $55B arbitrage: global F&A outsourcing market growth and delivery geography

Left: global F&A outsourcing market ($B), 2018-2030 forecast. Right: delivery geography by share of outsourced operations, 2025. India handles 38% of global FAO. Asia-Pacific accounts for 46% of global delivery capacity. Data: Grand View Research, Mordor Intelligence, Everest Group, THO Strategic Intelligence.

The global professional services market has not been waiting for a solution to the developed-world talent crisis. It has been building one for twenty years. And that solution has a clear geography: India and the Philippines.

India’s Global Capability Centres now host more than 1.6 million finance professionals. India handles approximately 38% of global Finance & Accounting outsourcing operations, processing hundreds of millions of transactions annually through firms including Infosys, Genpact, Wipro, and Capgemini. The India F&A BPO market generated $2.6 billion in 2024 and is projected to reach $4.9 billion by 2030 at an 11% CAGR. RSM US has already announced plans to more than double its Indian workforce to 5,000 employees to compensate for a 10% decline in its US accountant base.

The Philippines has built the world’s second-largest outsourcing delivery infrastructure. With 200,000 certified public accountants and a CPA Licensure Exam that produces around 8,200 qualified graduates annually, the country has positioned itself as the English-speaking, culturally Western-aligned alternative to India for US, UK, Australian, and New Zealand clients. The BFSI sector commands over 25% of Philippines BPO market share. Firms that outsource to the Philippines typically report 70% labour cost savings against domestic equivalents.

|

THE COMPETITIVE POSITION NIGERIA ENTERS These are the supply-chain incumbents. India and the Philippines built their F&A outsourcing dominance over twenty years of investment in professional education, digital infrastructure, and regulatory alignment with international standards. Nigeria’s tax reform does not replace this infrastructure — it opens a new lane. The strategic question for executives is not “India or Nigeria?” It is: “How do we build a globally distributed talent architecture that draws from all credible pools?” Nigeria offers a demographically young, English-speaking, common-law-trained population of 220 million — and a government now explicitly aligned with facilitating its professional workforce’s global participation. |

The global F&A outsourcing market stood at $54.79 billion in 2025, projected to reach $81.25 billion by 2030 at an 8.21% CAGR. North America commands 41.37% of this market as the dominant buyer. Asia-Pacific is the dominant supplier, growing at 9.3% CAGR. Eastern Europe and Latin America — particularly Mexico, Costa Rica, and Poland — constitute a third tier of nearshore supply for European and North American clients sensitive to data sovereignty and time zone considerations.

Critically, the outsourcing market is evolving from pure labour arbitrage toward capability arbitrage. India’s leading providers have advanced from transactional processing into controlling, treasury analytics, and strategic advisory. Firms like Capgemini and Cognizant are investing heavily in AI-driven platforms that combine offshore human expertise with machine processing. The future competitive advantage will not be found in whichever geography offers the cheapest accountant — it will be found in whichever geography develops the deepest combination of qualified judgement and AI-augmented tooling.

| FOR PRIVATE SECTOR EXECUTIVES Any organisation that has not yet conducted a structured assessment of its India and Philippines talent options is behind the curve. These markets are not theoretical alternatives — they are already the structural baseline for 75% of Fortune 500 companies in at least one finance function.The hybrid model — onshore senior oversight combined with offshore execution — is now the market norm, not a cost-cutting measure. Governance frameworks must be designed for this model as a permanent operating architecture, with IP, data residency, and professional indemnity structured accordingly.Nigeria now merits inclusion in any global talent sourcing strategy alongside India and the Philippines. The credential pathway (ICAN qualification, with ACCA and CPA routes increasingly available) requires due diligence, but the regulatory friction has been explicitly removed by the 2025 reforms. | FOR PUBLIC SECTOR EXECUTIVES Governments in high-shortage markets (Australia, UK, Canada) must update public procurement frameworks to accommodate and properly govern internationally distributed professional service delivery — including clear standards for data sovereignty, professional indemnity, and quality assurance.Development finance institutions should examine India and Philippines as governance models for how to build sovereign professional services capacity in developing economies. Both cases demonstrate that deliberate investment in professional education infrastructure creates durable global export capability.For African and emerging market governments: the lesson of India and the Philippines is that the window for building global professional services capacity is long but not permanent. Nigeria’s tax reform is necessary but not sufficient — infrastructure, credential reciprocity, and rule of law must follow. |

SECTION 03 | THE AI PARADOX

Two contradictory realities — and why both are true

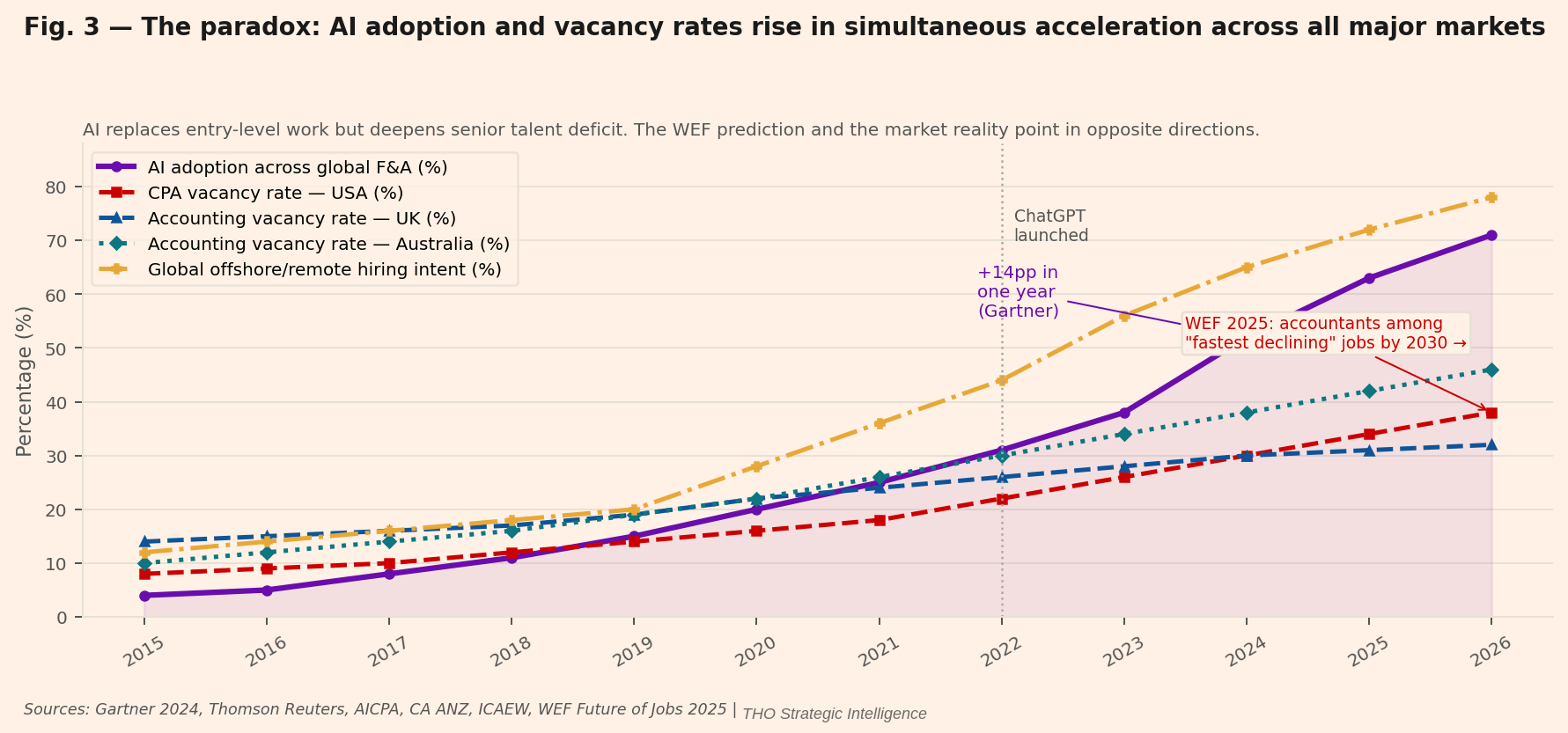

Fig. 3 The paradox: AI adoption and vacancy rates rise simultaneously across all major markets, 2015–2026

AI adoption across global F&A (purple); CPA/accounting vacancy rates for USA (red), UK (blue), Australia (teal); global offshore/remote hiring intent (amber). All rise simultaneously. The WEF 2025 prediction of “fastest declining” status is annotated. Data: Gartner, Thomson Reuters, AICPA, CA ANZ, ICAEW, WEF Future of Jobs 2025, THO Strategic Intelligence.

The World Economic Forum’s Future of Jobs Report 2025 places accountants and auditors among the twenty occupations expected to decline fastest globally by 2030. Accounting, bookkeeping, and payroll clerks rank seventh on the list of fastest-declining roles, with a projected 20% decrease in headcount. AI, information processing technologies, and broadening digital access are cited as the primary drivers. The WEF surveyed 1,043 companies across 55 countries to reach these conclusions.

These projections are simultaneously correct and deeply misleading — and understanding the distinction between them is one of the most important analytical tasks facing strategic leaders today.

|

THE DISTINCTION THAT MATTERS The WEF is correct that routine accounting roles — bookkeeping, accounts payable and receivable, payroll processing, data entry — will be substantially automated by 2030. Thomson Reuters confirms that 52% of accounting firm staff already use open-source generative AI tools. AI adoption across global finance functions reached 52-58% in 2024. These lower-skilled transactional roles will decline. What the WEF conflates is “accounting as data processing” with “accounting as professional judgement.” The vacancy crisis is not in data-processing roles. It is in the professional judgement roles that are getting harder to fill as AI eliminates the apprenticeship pathway through which that judgement was historically formed. |

The entry-level analyst who spent three years doing tedious reconciliations was not wasting their time. They were accumulating the forensic pattern recognition that eventually allows a senior partner to identify when figures are technically correct but commercially implausible. AI is automating exactly those reconciliation tasks — and in doing so, eliminating the training ground through which the next cohort of senior professionals would have developed their judgement. The WEF prediction and the vacancy crisis are both real. They describe different layers of the same profession.

The strategic question for boards is not: “Are we using AI efficiently?” It is: “What is our plan for maintaining senior professional judgement capacity in a world where AI has automated the apprenticeship?”

| RISK: THE FALSE EFFICIENCY GAIN Organisations that optimise AI efficiency today without rebuilding professional development pipelines are trading present productivity for future governance risk. The senior partner whose judgement validates AI output is a finite, non-renewable resource in the current demographic.Compressed senior-to-junior ratios and AI-generated work product without sufficient human review represent rising material misstatement risk — a risk that audit committees in all six shortage markets must price explicitly into their risk registers.The WEF’s 20% decline forecast for bookkeeping/payroll clerks is accurate. But those roles were the training ground for the profession’s future senior practitioners. Eliminating them without providing an alternative development pathway is a governance time bomb. | OPPORTUNITY: THE COUNTER-CYCLICAL ADVANTAGE Firms in any market that invest counter-cyclically in structured human development alongside AI adoption will build durable competitive advantage as the judgement deficit becomes visible industry-wide within 5-7 years.Australia’s CA ANZ notes that 92% of organisations are looking to reskill and upskill their workforce to integrate AI. The firms that move from aspiration to structured programme will separate from the field.AI-augmented apprenticeship models — where AI handles the mechanical work but junior professionals are deliberately assigned judgement-intensive tasks — represent the most promising structural innovation in professional services talent development currently being piloted. |

SECTION 04 | THE NIGERIA FACTOR

A sovereign policy innovation in a market shaped by incumbents

Nigeria’s position in this story must be understood in the context of the incumbents it is challenging. India and the Philippines built their global professional services supply infrastructure over two decades. Nigeria’s 2025 Tax Reform Acts represent a deliberate policy attempt to enter that market — not by replicating India’s model, but by leveraging the specific regulatory advantage that no other country has yet deployed: the explicit fiscal liberation of diaspora professional labour.

On 26 June 2025, President Bola Tinubu signed four major Tax Reform Acts into law — the Nigeria Tax Act, the Tax Administration Act, the Nigeria Revenue Service Act, and the Joint Revenue Board Act — taking effect 1 January 2026. The Presidential Fiscal Policy and Tax Reforms Committee subsequently clarified that diaspora Nigerians not tax resident in Nigeria — defined as spending fewer than 183 days in Nigeria in a 12-month period — are not taxed on foreign employment or business income. Income earned abroad and remitted to Nigeria is specifically exempted regardless of whether tax was paid in the country of work.

|

WHAT THIS MEANS IN PRACTICE — AND WHAT IT DOES NOT A Nigerian-qualified accountant working remotely for a UK firm while residing in Lagos: no incremental Nigerian tax on those earnings. A Nigerian-trained lawyer providing legal advisory to a Canadian company via video conference: no Nigerian tax obligation. The friction of cross-border professional employment has been deliberately removed on the supply side. What remains — and what executives considering Nigerian talent must evaluate carefully — is credential reciprocity. A qualification under the Institute of Chartered Accountants of Nigeria (ICAN) is not automatically a US CPA or UK ICAEW qualification. The professional credential pathway requires assessment and, in many cases, additional examination. Firms should not assume that fiscal liberalisation resolves the credential equivalence question. |

Nigeria is a country of 220 million people, producing tens of thousands of accounting, legal, financial, and technology graduates annually. Its professionals are English-speaking, trained under a common-law legal framework, and aligned with IFRS-based reporting standards. Nigerian professionals have historically been lost to permanent physical emigration — a one-way transfer of human capital that returned nothing to the domestic economy. The 2025 reforms represent a deliberate policy shift: Nigeria is no longer competing to retain professionals physically. It is competing to retain them economically, socially, and fiscally — betting that professionals embedded in Nigerian society, even while earning internationally, will invest, consume, and sustain the economic fabric of home.

For the global professional services market, this creates a new tier of supply that did not previously exist in a formally accessible form. Whether Nigeria can develop from a policy innovation to a credible supply infrastructure of the scale that India and the Philippines have built is a question of execution over a decade, not a question resolved by a single legislative act. The practical prerequisites — reliable digital connectivity, professional credential reciprocity frameworks with major markets, a stable regulatory environment for data-sensitive work, and the professional indemnity architecture that firms require — remain works in progress.

| FOR PRIVATE SECTOR LEADERS Nigeria should be assessed as a talent market opportunity with a defined credential due-diligence requirement — not dismissed for lack of ICAN-to-CPA automatic equivalence, but also not treated as a turnkey solution equivalent to an established India or Philippines provider.The practical entry point for most organisations is through hybrid arrangements: Nigerian professionals qualified under ACCA (internationally portable) or in the process of sitting US CPA or UK ICAEW exams, working within a governance framework designed for international remote professional employment.Firms should conduct a comprehensive assessment of employer obligations in international remote arrangements — payroll structure, IP ownership, data residency, professional indemnity coverage — before committing to a Nigerian talent strategy. The tax reform clarifies the employee’s obligation; the employer’s obligations remain the hiring organisation’s responsibility. | FOR PUBLIC SECTOR LEADERS For Nigerian policymakers: fiscal liberalisation is a necessary first move, not a complete strategy. The 183-day rule requires consistent and transparent enforcement to build employer confidence. Infrastructure investment — power, connectivity, data sovereignty frameworks — and formal credential reciprocity agreements with major markets are the next policy priorities.For high-income market governments: Nigeria’s reform is the first significant sovereign move in a new global talent economics. Bilateral frameworks for professional recognition, employment law, and data governance between high-income shortage markets and high-supply emerging economies are increasingly urgent. The absence of such frameworks imposes compliance costs that reduce the incentive to draw on these talent pools.For development finance institutions: Nigeria’s model merits formal evaluation as a replicable template for other high-emigration, high-graduate-output economies seeking to harness diaspora earnings without permanently losing their professional class. |

SECTION 05 | THE CONVERGENCE

Four forces, six markets, one structural reordering

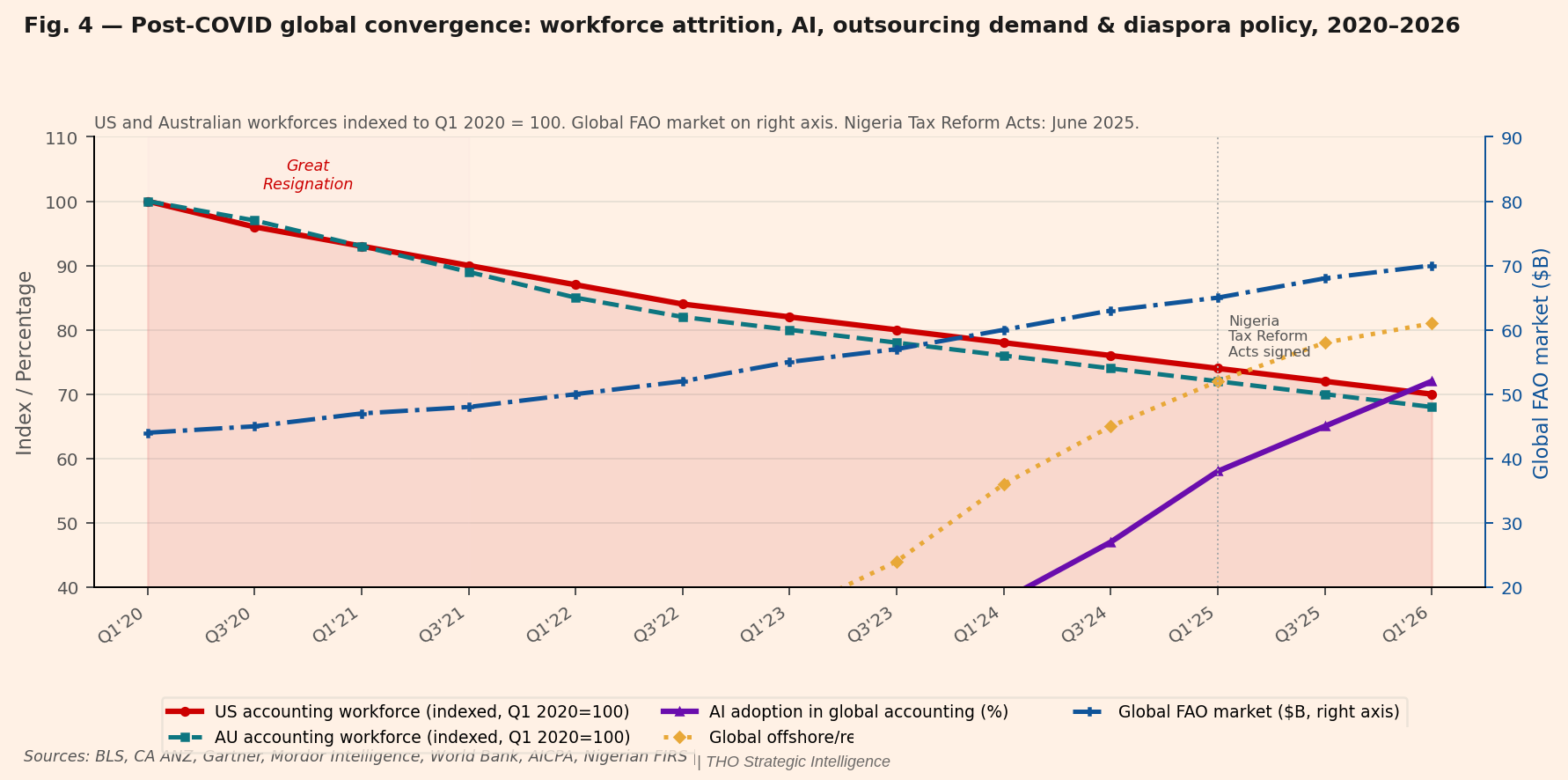

Fig. 4 Post-COVID global convergence: workforce attrition, AI adoption, outsourcing demand & diaspora policy, 2020–2026

US and Australian workforces indexed to Q1 2020=100. AI adoption and offshore hiring intent as % of firms. Global FAO market ($B) on right axis. Nigeria Tax Reform Acts signed June 2025. Data: BLS, CA ANZ, Gartner, Mordor Intelligence, World Bank, AICPA, Nigerian FIRS, THO Strategic Intelligence.

The post-COVID quarterly chart shows the velocity at which four distinct structural forces pivoted simultaneously and began to compound. The Great Resignation drained professional accounting workforces in every high-income market between 2020 and 2023 — over 300,000 in the US alone, with proportionate losses in the UK, Australia, and Canada. AI adoption in finance functions doubled between 2022 and 2024. Global offshore hiring intent rose from 35% to over 80% of surveyed firms. And the global F&A outsourcing market grew from $44 billion in 2020 to $55 billion in 2025, with the trajectory toward $81 billion by 2030 showing no sign of deceleration.

The compounding effect is what distinguishes this period from previous cycles of professional services disruption. An organisation that lost accounting staff to resignation in 2021, adopted AI tools to cover the gap in 2022, began offshore outsourcing to manage costs in 2023, and is now recruiting internationally in 2025 has not solved its structural challenge. It has deferred it — while accumulating governance complexity at each stage — and each layer of that complexity requires senior professional oversight that is itself increasingly scarce.

|

THE BOARD-LEVEL DIAGNOSTIC Does your organisation have explicit board-level visibility of: (a) your current ratio of AI-generated to human-reviewed financial work product across all jurisdictions; (b) the seniority profile of your remaining professional finance staff and the retirement exposure within five years; (c) a documented and stress-tested plan for the three months following the departure of your three most senior finance professionals; and (d) the credential equivalence status of every internationally-sourced member of your finance function? If not, you are carrying governance exposure that is not yet priced in your risk register. |

SECTION 06 | STRATEGIC IMPERATIVES

Decisions required now — by function and jurisdiction

For Private Sector Executives

| 1 | Build a global talent architecture, not a domestic hiring plan [ CEO, CFO, CHRO, Board ] Commission a structured review of your professional services talent strategy across all jurisdictions in which you operate. Model three scenarios: domestic supply stable, domestic supply -25%, domestic supply -50%. The middle scenario is already reality in Australia; the third is directionally correct for the US. |

| 2 | Conduct India and Philippines market entry assessments within 90 days [ CFO, COO, Head of Finance Operations ] If you do not have an established offshore F&A capability in India or the Philippines, you are already behind 75% of Fortune 500 peers. Assess providers, governance frameworks, and credential verification processes. RSM US’s decision to double its Indian workforce to 5,000 is a directional signal, not an outlier. |

| 3 | Include Nigeria in your global talent pipeline — with credential due diligence [ CFO, Head of Tax/Audit, Legal Counsel ] Develop a Nigerian talent market entry position: assess ICAN-to-target-market credential pathways, identify ACCA-qualified Nigerian professionals, and design a compliant remote employment framework addressing IP, data residency, and professional indemnity. The fiscal friction has been removed; the operational framework is your responsibility. |

| 4 | Establish an AI governance standard before the deficit becomes visible in your accounts [ CFO, General Counsel, Audit Committee Chair ] Define and document the human oversight threshold below which AI-generated financial work product requires independent professional review. Make this threshold explicit in audit committee mandates. The Advance Auto Parts material weakness event is not an anomaly — it is a preview. |

| 5 | Invest counter-cyclically in human professional development [ CHRO, CFO, Professional Services Leadership ] Design AI-augmented apprenticeship tracks that preserve the judgement-formation function of entry-level roles even as their mechanical content is automated. Firms that do this in the next three years will have a senior talent bench that peers will lack by 2030. |

| 6 | Price talent scarcity into long-term financial projections [ CEO, CFO, Board Finance Committee ] Finance function costs will increase materially through the decade in all six shortage markets. Salary inflation, offshore premium, governance complexity, and AI investment combine into a cost trajectory that must be modelled into margin projections and capital allocation decisions — not treated as a variable to be optimised away. |

For Government and Public Sector Leaders

| 1 | Declare accounting a sovereign infrastructure priority — not a market signal [ Finance Ministries, Treasury, Education Departments ] Ireland has. Australia’s CA ANZ is formally requesting it. The UK’s Skills England has effectively done so. The US has not. Revenue enforcement capacity, audit quality, and financial stability all rest on a professional workforce that is now formally in shortage. Policy intervention — on qualification barriers, cost of entry, and salary bands — is warranted. |

| 2 | Conduct a formal workforce vulnerability assessment for all public finance functions [ National Audit Offices, Finance Ministries, Civil Service HR ] Revenue agencies, national audit offices, comptrollers, and central banks must model the retirement exposure in their own professional finance staff and assess the gap between current talent pipelines and required capacity through 2030. This assessment is overdue in every G7 economy. |

| 3 | Develop bilateral frameworks for cross-border professional services — urgently [ Foreign Affairs, Trade Departments, Finance Ministries ] The existing international frameworks for professional recognition and remote employment were not designed for a world in which 38% of global accounting operations are delivered from India and a new African sovereign policy is deliberately opening cross-border professional employment. Bilateral agreements on credential reciprocity, data governance, and employment law need modernisation — now. |

| 4 | Commission an AI governance standard for public finance functions [ National Audit Offices, Digital Government, Finance Ministries ] Governments deploying AI in tax processing, audit verification, and financial management without defined human oversight thresholds are creating systemic audit risk in their own accounts. A cross-government AI governance standard for finance functions is a near-term legislative and regulatory priority. |

| 5 | Study and co-design Nigeria’s diaspora model as a G20 policy framework [ G20 Finance Ministers, IMF, World Bank, OECD ] Nigeria’s Tax Reform Acts represent the first sovereign use of fiscal policy to facilitate diaspora professional labour participation without permanent emigration. For G20 finance ministers, this warrants serious study as a template that other high-graduate, high-emigration economies may replicate — and as a model that requires bilateral framework support from high-income markets to reach its potential. |

The Reckoning

In a Lagos apartment, a Nigerian-qualified accountant is reviewing a contract from a UK audit firm. In Manila, a CPA is finalising the year-end accounts of an Australian manufacturer. In Bangalore, a finance analyst is running the accounts payable operation of a Fortune 500 company whose CFO is based in New York and has not met a full accounting team in three years. In Nottingham, a regional accounting firm has two applicants for every role it posts. In Washington, the IRS is modelling what happens to enforcement capacity if its accountant vacancy rate continues to compound. In Canberra, CA ANZ is drafting its third consecutive urgent submission to the government asking for accountants to be added to the national skills shortage list.

These are not separate stories. They are one story, playing out simultaneously across six continents, in every high-income economy, at the precise moment that the technology that was supposed to solve the problem is instead eliminating the pathway through which the next generation of professionals would have qualified to solve it themselves.

|

THE STRATEGIC REALITY The professional services workforce — accountants, auditors, tax professionals, financial analysts — is the connective tissue of modern market economies. It is what makes capital markets legible, tax systems enforceable, and corporate governance meaningful. That tissue is thinning, simultaneously, everywhere. Leaders who act on this convergence now — redesigning talent architecture, governance frameworks, and international sourcing partnerships for a structurally different professional landscape — will be materially better positioned than those who wait for the deficit to appear in their own audit findings. The ledger does not balance. The question is who takes responsibility for reconciling it. |

Data Sources & Methodology

United States: AICPA, NASBA Candidate Performance Reports 2005-2024, Bureau of Labor Statistics Current Employment Statistics. United Kingdom: ICAEW, ACCA, CIMA via FRC Key Facts & Trends Report; Skills England Skills Assessment September 2024; Accountancy Age; Robert Half UK Salary Guide. Australia: CA ANZ Occupation Shortage Survey 2024, Chartered Accountants ANZ, CPA Australia, HECS data, ABS projections. Canada: CPA Canada, BNN Bloomberg April 2024, Robert Half Canada. Ireland: CPA Ireland, Government Critical Skills List 2022. Philippines: CPA Philippines (PRC data), Commission on Higher Education, Robert Walters Philippines. India: Grand View Research India F&A BPO Market Outlook 2025-2030; Mordor Intelligence Finance & Accounting Outsourcing Market 2025. Global outsourcing: Grand View Research Global F&A BPO Market $64.9B estimate 2024; Mordor Intelligence $54.79B 2025 base; Everest Group Finance & Accounting Outsourcing Annual Report 2025-2026. AI adoption: Gartner CFO & Finance Function Survey 2024; Thomson Reuters Future of Professionals 2025. WEF: Future of Jobs Report 2025 (1,043 companies, 55 countries); WEF Four Futures for Jobs in the New Economy 2025. Nigeria: Presidential Fiscal Policy & Tax Reforms Committee official guidance January 2026; FIRS clarification notes. Nigeria remittances: World Bank Migration & Development Brief 2025. Note: Where market sizing estimates vary across sources, the text uses the midpoint or most methodologically conservative estimate and identifies the source. Historical workforce interpolations use linear regression between known data points from cited sources.